In today’s dynamic investment landscape, it is increasingly challenging for active managers to provide the alpha many investors seek from their core equity holdings. With thousands of stocks to choose from, human capacity is limited in evaluating opportunities for both overperformance (going long) and underperformance (short selling). This is where experienced quantitative managers, like the Mackenzie Global Quantitative Equity (GQE) Team, demonstrate their strength. To capitalize on alternative strategies such as long/short, or “alpha extension,” the team employs a quantitative approach to express their views on the US markets by taking active long and short positions. Their methodology, reflected in their impressive track record, highlights their ability to navigate the complexities of the market and generate consistent alpha.

The Mackenzie GQE Team employs a systematic, factor-based model that uses four “super factors” — value, growth, quality and informed market participant activity — to rank securities daily. This holistic and core-style approach ensures balanced exposure across different investment styles. The weights of these factors are determined through historical analysis and are tailored based on the specific characteristics of individual stocks. Additionally, the team adjusts the weights of factors differently for long and short positions to optimize the model's predictive power.

This asymmetrical weighting of factors is a key aspect of the team's strategy. By recognizing that certain factors may have different success rates in short positions compared to long positions, the team can better predict which stocks are likely to outperform or underperform. This enhances the overall effectiveness of their predictive model and improves risk-adjusted returns.

Evidence of excess return

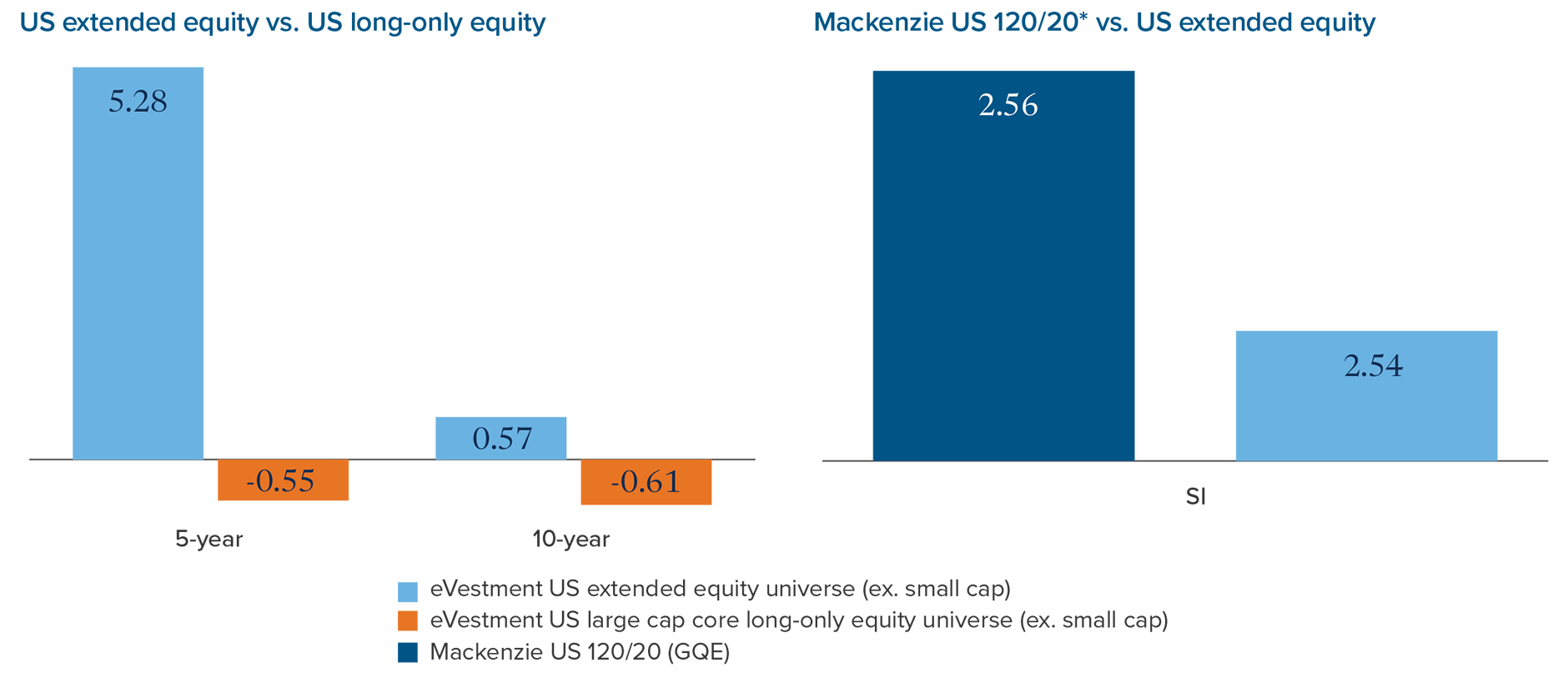

On average, the team’s simulated model has delivered strong returns in both the top and bottom deciles across the four proprietary super factors in their stock selection model (Figure 1). This suggests the GQE process has been successful at uncovering alpha potential in both long and short security selection over time. Figure 2 summarizes the median excess return (net of fees) between the eVestment US extension equity and the eVestment US large cap long-only equity universes. It also highlights the performance of the GQE Team’s institutional Quantitative US Core Extended Equity (120/20) strategy and how it has produced superior alpha above the extended equity universe.

Throughout all time periods presented below, the median excess return of US extended equity strategies consistently outperformed that of US large-cap long-only. This suggests that amplifying a core US equity portfolio with an actively managed quantitative alpha extension strategy can be an effective way to remain fully invested in US equities.

Figure 1. Simulated model performance of “super factors” *

Source: Mackenzie Investments. Represents univariate factor performance of Mackenzie’s Quantitative US Core Extended Equity model based on simulations from January 1997 – December 2024, the full data timeframe available.

The positive values on the left of the table show the alpha generated by the Mackenzie GQE Team’s super factors over the top decile of performers in the GQE model’s US large cap universe. The negative numbers on the right show the positive alpha created from short selling the bottom decile of the GQE model’s US large cap universe. Together it shows how the team has been able to generate alpha from both long and short positions over time.

Figure 2. Median excess return, based on eVestment universe

By targeting strong risk-adjusted excess returns while maintaining a similar overall market exposure, these strategies can be particularly effective within the US large-cap universe, where markets are most efficient.

To capitalize on the additional alpha potential, it is crucial to identify active managers who consistently add value through successful stock selection, disciplined risk management, and experience in managing costs, risks and operational challenges.

The Mackenzie GQE Team’s quantitative approach exploits market inefficiencies by leveraging evolving alpha signals to identify attractive long and short opportunities. They apply stringent risk constraints, supported by extensive back testing, and partner with experienced prime brokers to mitigate counterparty and liquidity risks.

Their extension strategies aim to deliver additional alpha compared to long-only strategies while maintaining similar risk levels (tracking error). By improving the information ratio without introducing uncompensated risk, they believe this approach is well-suited for today’s environment and offers a solution for investors seeking alternatives to passive or constrained long-only strategies.

*Hypothetical performance is for illustrative purposes only. It should not be interpreted as an indication or guarantee of future results. Actual performance of the Fund may vary significantly. The portfolio of the Fund will generally include securities that are included in the Quantitative US Core Extended Equity (the “Private Fund”) which was launched on August 3, 2020. However, the Private Fund is available only to accredited investors. As such, the Fund will slightly differ from the Private Fund and no representation is being made that an actual investment in the Fund is likely to achieve similar returns to the historical returns of the Private Fund. The Private Fund’s historical performance does not include the impact of fees, commissions and expenses that would be payable by investors of the Fund. The Private Fund’s performance is not an exact illustration of how this Fund will perform. The Fund will act as a sister fund to the Private Fund with slight differences stemming from timing of subscriptions and redemptions, and trading considerations regarding lots and transaction costs which may impact position weights between the two portfolios.

For advisor use only. No portion of this communication may be reproduced or distributed to the public, as it does not comply with investor sales communication rules. Mackenzie disclaims any responsibility for any advisor sharing this with investors.

Gross composite returns do not reflect the deduction of advisory fees. Returns are net of transaction costs but do not include the deduction of custody fees or other (non-advisory) costs, fees and expenses that may be incurred in managing an investment account. A portfolio’s return will be reduced by costs, fees and expenses and their impact can be material. Returns assume the reinvestment of dividends, interest, and realized and unrealized capital gains and losses. Index returns do not reflect transaction costs, or the deduction of other fees and expenses and it is not possible to invest directly in an index. Further details on Transaction Costs or estimated dividend withholding taxes is available upon request.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this document (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 4, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.